Like the previous quarters of the calendar year 2012, the last quarter ending December too finished off in positive. Issues surrounding the financial health in both US and Euro-zone pretty much dictated the markets trends globally this quarter. And despite events back home being quite supportive to the market sentiment, the global influence on the overall market movement could not be negated. The quarter started off on a negative note but thereon it kept a strong holding to finally end the quarter with decent gains.

Volatility ruled the markets throughout the quarter with markets losing ground towards the start i.e in the month of October. This fall happened mainly as global stocks fell after resurfacing of euro-zone debt worries and on dimming hopes of further US quantitative easing. Back home warning by global ratings agency Standard & Poor’s (S&P) of a significant chance of downgrading India’s debt rating in the future severely dented sentiments. Further, a disappointing start to earnings season, declining exports data, rising inflation and the resultant inaction by the central bank to cut interest rates worked against the markets. What spooked the markets further was lowering of economic growth forecast to 5.8% for 2012-13, from 6.5% projected earlier by the government.

While the month of October turned out to be a clumsy one, markets returned back to action in November despite the odds. Where on one hand the markets cheered the re-lection of US President Barak Obama for yet another term, concerns over US “fiscal cliff”, Europe's long-drawn debt problems and weak macro-economic data back home kept investor sentiments on the edge. It was towards the end of the month when the equity indices soared higher following a series of positive news flowing in from both global and domestic markets. Events like rating agency Moody’s retaining a stable outlook on India’s debt rating, political stability relating to the FDI issue and strong foreign fund inflows supported markets on the domestic front. Globally too news that that Greece's official creditors agreed on a deal to lower the country's debt burden along with growing possibility of US President Barack Obama being able to strike a deal with Congressional leaders over budgetary reforms to avert the upcoming fiscal challenges supported markets sentiments.

The final month of the quarter too saw a bumpy ride for the market as it just about managed to hold its head above the water. While things remained quite neutral on the domestic front except the increasing trade deficit and yet another disappointment by the Reserve Bank of India (RBI), it was primarily the global issues that worried the markets. Sustained worries about U.S. fiscal challenges weakened investor confidence in December. But again ECB’s new bond buying program announcement to help troubled economies helped ease concerns related to the US fiscal cliff.

On the macro-economic front things were quite mixed. While the quarter saw improvement in both industrial production and inflation, rising trade deficit due to slowing exports and a slowing economic growth raised eyebrows. IIP which had seen contraction of 0.7% as per the data released for September witnessed a strong growth of 8.2% for the month of October. Similarly the WPI inflation was seen easing from 7.81% in September to 7.24% in November. However the GDP slowed down to 5.3% as compared to 5.5% in the previous quarter. In the light of the same, the RBI kept its stance quite conservative as it decided to keep rates unchanged as against the market expectation of rate cuts. However it did raise some optimism on hopes that the central bank might consider cutting rates in the next year review.

Overall the markets which began the quarter on a weak note gathered momentum towards the end to finally end the quarter with strong gains.

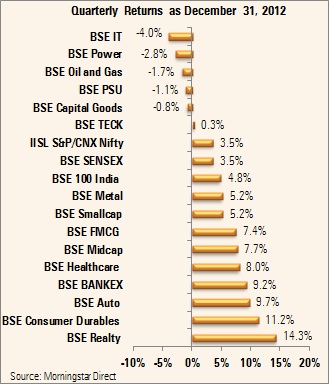

During the quarter, the BSE Sensex crossed the 19,000 mark as it touched a high of 19,486 and a low of 18,309 before it ended 3.5% higher to close at 19,426. Similarly the S&P CNX Nifty managed to soar above the 5,900 mark before closing 3.5% higher at 5,905. The mid cap and small cap stocks witnessed strong growth during the quarter thereby outperforming their large cap peers. Both the BSE Mid-cap and BSE Small-cap indices gained 7.7% and 5.2% respectively.

It was a mixed bag performance on the BSE sectoral front. The BSE Realty index emerged as the highest gainer which grew by 14.3% recording its highest gain in the month of November. Within this space, the stocks which contributed the most to the overall gain was D.B.Realty, Unitech International and Prestige Estate which each grew by 119%, 38% and 32%. The index heavyweight, DLF, on the other hand lost 1.1% during the quarter.

This was closely followed by the BSE consumer Durable index which gained 11%. Interest rate sensitive stocks too grew on hopes of rate cut. The BSE Auto and BSE Bankex indices each gained 9.7% and 9.2% respectively.

The defensives followed next with both the BSE Healthcare and BSE FMCG soaring 8% and 7.4% respectively. The healthcare stocks remained in positive throughout the quarter while the FMCG stocks witnessed some easing in the month of December.

On the other hand, the BSE IT index emerged as the highest loser which shed 4%. The stocks that fell the most within this space were Hexaware Technologies, Infosys and Mpasis which each shed 29%, 8% and 4.5% respectively.

Among the other key losers on the BSE sectoral space were BSE Power, BSE Oil & Gas and BSE PSU indices which each dropped by 2.8%, 1.7% and 1.1% respectively.

As per the data released by SEBI, foreign institutional investors (FIIs) have been strong buyers in equity for the quarter ending December 2012 which too contributed in supporting the jittery markets. The bought equities worth Rs 46,029 crores in the last quarter of calendar year 2012 making it the highest quarterly inflow in 2012. Similarly they net buyers in debt segment to the extent of Rs 9,847 crores for the quarter. Unlike the previous year 2011 when the FIIs were net sellers for the whole year, they were net buyers in equity in 2012 to the extent of Rs 120,925 crores.