In a bid to pass on the economies of scale to investors, the market regulator Securities and Exchange Board of India, or SEBI, has reduced the expense ratio of funds across categories.

The expense ratio slabs were introduced in 1996 and have not been altered since then, which means that the expenses have not reduced commensurate with the growth of the industry; from Rs 79,501 crore in July 1999 to Rs 25.20 lakh crore in August 2018. That translates into a compounded annual growth rate (CAGR) of 20%!

Modification in slab wise limits for Total Expense Ratios (TER)

SEBI has passed on the economies of scale of increasing asset size to investors. To this effect, they have modified the slab wise limits for TER of open-ended funds for equity-oriented funds as well as “other” funds. With this move we will see a reduction in TERs of most equity funds, while “other than equity oriented” funds will see limited reduction in TERs as most funds were already well within the maximum allowable limits.

Equity Oriented Funds

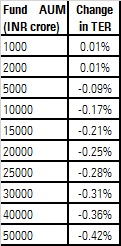

The introduction of new slabs with a lower TER limits will result in a reduction of overall TER of equity- oriented funds with assets greater than Rs 2,000 crore. Funds with assets size of less than Rs 2,000 crore will continue to have a similar TER as before. Most equity funds so far were charging the maximum allowable TER as per the erstwhile prescribed slabs. Therefore, with the introduction of new slab wise limits, TERs of most equity funds will reduce.

With increasing fund sizes, the quantum of reduction in TER increases. For instance, this move will result in a reduction of 9bps in the TER of a fund with an AUM of Rs 5,000 crore, but a fund with an AUM of Rs 20,000 crore will witness a reduction of TER to the tune of 28 bps. This is exactly what SEBI is trying to achieve, to pass on the economies of scale of larger funds to investors.

Below is the projected reduction in TER with the change in the slab wise limits for TER:

Other than equity-oriented funds

SEBI has also modified the slab wise limits for TERs of other than equity-oriented funds. It is important to note that majority of these funds charged TERs well within the maximum allowable limits. Thus, the impact of these changes in the slab wise limits for TER will be limited to only those funds whose TER was closer to the maximum allowable TER as per the erstwhile slab wise limits.

This recent reduction in slab wise limits coupled with the earlier reduction in additional TER that could be charged in lieu of exit loads (from 20 bps to 5 bps) and the change in the additional TER chargeable for payouts for inflows from B-15 cities to B-30 cities should result in a meaningful reduction in overall TERs of equity funds in the range of 20-50 bps per annum depending on the size of the fund.

Rationalization of commission structure

Bringing more transparency and clarity on the payout of commissions to distributors by fund houses, SEBI has directed the industry to adopt a full trail model in all schemes (except for SIPs) without payment of any upfront commission or upfronting of any trail commission.

Industry body AMFI had laid down best practice guidelines for fund houses with respect to the payment of upfront and trail commission to distributors. Some of the salient features of the guidelines were – for the first year, the upfront commission was capped at 1%; the upfront commission plus trail commission must not exceed the total expense ratio; and the trail commission for the subsequent years cannot be higher than the first year. Though rightly intended, these guidelines were not able to fully plug the loopholes. It left scope for distributors to increase churn in investors’ portfolio leading to conflict of interest.

However, with this new diktat by SEBI, the upfront commission regime has come to an end in the Indian mutual fund industry. We believe, such a structure offers a win-win for all the stakeholders. This move will also encourage distributors to instill long-term investing culture among investors. Interestingly, many distributors have already started moving towards an all-trail model.

Although in case of SIPs, SEBI has left a scope for upfronting of trail commission subject to fulfilment of certain conditions. In our opinion, that is done in order to promote the investments through SIPs, which unarguably is the most disciplined way of investing.

Additional expenses of 30 bps for penetration in B-30 cities

With regard to the additional expense that can be charged by funds for penetration in B-30 cities, SEBI has stated that this expense can only be charged for inflows from retail investors and not inflows from corporates or institutions. The definition of retail investors would be determined in consultation with the industry. Excluding corporate and institutional inflows is a step in the right direction, as it can be assumed that these entities are better informed/regular mutual fund investors. The impact on expense ratios across equity and fixed income categories would depend on the proportion of inflows from retail, corporate and institutions.

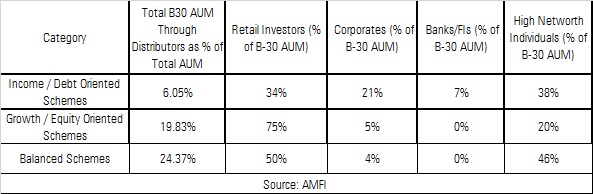

Data on inflows from B-30 locations isn’t readily available. Given below is the share of B-30 locations of overall AUM garnered through distributors and the proportion of B-30 AUM from retail, corporates, Banks/FIs and HNIs. Clearly, retail and HNI investors (as defined by AMFI) contribute to bulk of the assets from B-30 locations. Hence, the definition of retail investors would be important in determining the impact on expense ratios and whether HNIs would form part of retail investors. If retail and HNI are clubbed together then the impact of this change on the expense ratios might be limited based on AUM.

Impact on direct plans

The new AUM based expense ratio slabs would be applicable for direct plans as well, which should ideally result in a reduction of expense ratios for direct plans. Although the impact of changes in the commission payout structure (from upfront to all-trail) on the difference between regular and direct plan expense ratios remains to be seen. Currently, the guideline for determining expense ratios for direct plans states that the difference in expense ratios for regular and direct plans should reflect the commissions paid to distributors for the regular plan. Since SEBI has now disallowed upfront commissions and funds can now follow a all-trail model (except for SIPs) for commission payouts, the difference in the expense ratios for regular and direct plans would probably reflect the trail commissions paid out. No specific levels or caps on trail commissions have been defined, although upfronting of trail commissions has been disallowed.

Expenses on close-ended funds have been cut sharply

Till date, close-ended funds have enjoyed the same TER structure as that of open-ended funds. That has changed with the cut in TER charged on close-ended funds and capped at 1.25% for equity funds and 1% for schemes other than equity funds.

At Morningstar, we have never seen much merit in close-ended equity funds. Over the last few years, there has been a steady stream of close-ended equity fund launches. The recent guidelines around TERs will ensure that such funds are launched purely based on investment merit.

Impact on Commissions

With the reduction on overall TERs, it will be interesting to see how things pan out with respect to its large components - management fees and distributor commissions.

In our opinion, the benefits of increasing economies of scale exist with the asset management firm rather than with the distribution fraternity. Asset managers should follow this diktat in true spirit by not passing on the brunt to distributors.

Additionally, to reduce the overall cost to investors, GST needs to be reconsidered.