This article has been written by Larissa Fernand, Editor of Morningstar.in, and Himanshu Srivastava, Senior Fund Analyst.

When we reiterated our ‘Gold’ rating for HDFC Top 200 and HDFC Equity, we were taken aback by the stern criticism to our stance (see: 2 large-cap ‘Golds’ from HDFC Mutual Fund).

It was implied that our positive outlook on the funds indicated that we "did not want to mess with the market leader" and that we tried too hard to "justify Prashant Jain’s underperformance". While that was subjective, there were some technical aspects too, such as "why were both funds classified as large caps?"

Let’s be honest. We really did not expect everyone to be on the same page as us; on the contrary. But our concern is that the issues of contention centre on Morningstar’s core research principles, which we would like to elucidate upon.

Morningstar’s analyst team works independently and objectively. The AMCs position, as market leader or not, has absolutely no impact on the analysis of the individual fund.

What we do believe is that understanding a firm’s culture is paramount to predicting stability in its ranks. A firm’s culture is difficult to assess at any one point in time, but rather is a mosaic that you have to piece together over time through iterative, in-depth diligence.

The research should yield answers to questions like whether the firm is primarily focused on investing rather than asset-gathering and if portfolio managers have enough skin in the game through fund ownership.

In the case of HDFC AMC, roughly half of the manager pay is variable in nature and largely linked to performance. Appropriate time frames matching the strategy (such as 6 months, 1-2 years for fixed income funds and 3 years and the manager’s start date for equity funds) are considered to evaluate performance.

We believe that HDFC AMC is an excellent steward of investors’ capital. Its reputation has been built on a disciplined investment process and a consistent long-term focus.

The bone of contention amongst a number of our readers has been the fund’s performance this year.

We believe performance should be a single input into a process, not a divining rod. It really should play a confirmatory role. For instance, what does the fund's track record tell you about its investment style? What does it reveal about how the manager has executed his approach? Can you reconcile the way the fund has performed to the manager's stated investing discipline?

Because we view performance in the context of strategy and the manager’s intrinsic investment style, we may still be convinced about a good fund despite it hitting a roadblock.

In 2007, HDFC Top 200 and HDFC Equity underperformed the category average. That is because Jain stayed away from momentum stocks in infrastructure and real estate.

In 2013, his bets on Infosys and SBI did not pay off resulting in an underperformance that year. But this is typical of Jain’s style – he does not get deterred in his conviction, even if it means the funds slipping down the performance ladder for a year or so.

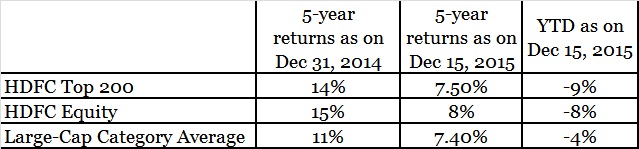

This calendar year has been particularly rough on the funds. His high conviction bets on banking stocks, such as SBI – his largest holding, have detracted from this year’s performance. This is evident when you look at the year-to-date returns. And it is this hit that has brought down the 5-year returns to a mere average.

Looking at performance in conjunction with his investment approach, our analysts have the confidence that this fund will continue to deliver over the long term.

HDFC Equity has completed 20 years and HDFC Top 200, 19 years. Both funds have put up some excellent numbers over this period as well as over a 10-year time frame. And while we have been accused of being “desperate to justify our stance by talking about the impressive performance over the long term,” we are blatantly unapologetic of the fact that equity investing must not be looked upon with an investment horizon of a few years. One has to take a 5-year view at the very least.

As for the technical aspect, there are various definitions as to what constitutes a large-cap stock. At Morningstar, large-cap stocks are defined as the group that accounts for the top 70% of the capitalisation of each geographic area. In the case of Morningstar India that would be Asia, ex-Japan.

As far as HDFC Top 200 is concerned, on an average over the past 5 years, 88% of the portfolio was cornered by large cap stocks. The figure stands at 74% in the case of HDFC Equity.

Conclusion

Morningstar evaluates funds based on five key pillars--Process, Performance, People, Parent, and Price--which its analysts believe lead to funds that are more likely to outperform over the long term on a risk-adjusted basis.

- Process: What is the fund's strategy and does management have a competitive advantage enabling it to execute the process well and consistently over time?

- Performance: Is the fund's performance pattern logical given its process? Has the fund earned its keep with strong risk-adjusted returns over relevant time periods?

- People: What is Morningstar's assessment of the manager's talent, tenure, and resources?

- Parent: What priorities prevail at the firm? Stewardship or salesmanship?

- Price: Is the fund a good value proposition compared with similar funds sold through similar channels?

This analyst rating is not a market call but is based on the analyst's conviction in the fund's ability to outperform its peer group and/or relevant benchmark on a risk-adjusted basis over the long term.

A Gold rating suggests the best-of-breed that distinguishes itself across the five pillars and has garnered the analysts' highest level of conviction. It means Morningstar analysts think highly of the fund and expect it to outperform over a full market cycle of at least 5 years.