Government bonds entered December under a favorable environment and with a positive outlook. After being under pressure for a larger part of the year--threatened by unabated inflationary pressures and consistently-rising interest rates--the turn of events towards the end of November indicated a change in trend.

Data released on November 30, 2011 showed gross domestic product growth fell to 6.9% in the second quarter of FY 2011-12 as against 7.7% in quarter-ended June 2011, thus logging below 8% for the third straight quarter.

This was Indian economy’s weakest pace of growth in more than two years. This highlighted the heavy damage that stubbornly high inflation, rising interest rates and crisis-hit global capital markets are having on Asia’s third-biggest economy.

Hence, after seeing a 225 bps hike in interest rates this year till November, investors in the fixed-income segment entered the last month of the year with hope that the RBI would pause on its rate-hike cycle, owing to the slowdown in the domestic economy.

Government bonds had a good run for larger part of the month, as their prices shot up sharply on the back of a series of positive cues emanating from domestic and global markets.

The most prominent was the central finally applying brakes to the rate-hike cycle. Bond prices were also boosted by open market operations (OMO) the RBI has been conducted from mid November to relieve persistent strain on systemic liquidity.

However, they lost steam towards the end of the month due to a bounding fear of a further increase in government borrowing before the end of this financial year.

Sentiment was also dampened by the improvement in risk appetite in global markets, wiping out most of the gains that government bonds clocked early in the month.

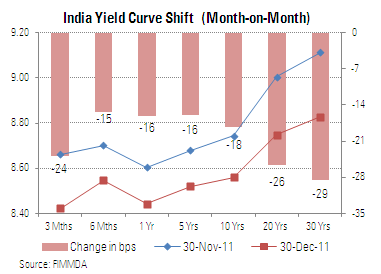

Yields on government bonds fell across board during the month on the back of a pause in interest rates and continuation of OMO.

While yields fell by 24 bps, 15 bps and 16 bps in the 3-month, 6-month and 1-year segments respectively; it fell in the range of 16 bps to 29 bps at the longer end of the yield curve.

The yield on the 10-year benchmark bond touched a low of 8.28% during the month before finally settling 18 bps lower at 8.56% from 8.74% on November 30, 2011.

Over a one-year period, yields continued to be at elevated levels, especially at the shorter-end of the yield curve.

Fresh from the sharp drop in GDP growth rate, government bonds started the month on a positive note with expectations that the slowdown in the economy would force RBI to apply brake on its rate hike cycle.

The hope was further fanned after the data released on December 12, 2011 showed that the industrial output contracted by 5.1% in October as against 1.9% growth in September.

Finally, as expected, RBI stayed true to its guidance given in October and kept key interest rates unchanged while announcing its mid-quarter monetary policy review on December 16.

Government bonds were also immensely benefitted by the continuation of RBI’s OMO to buy bonds in order to infuse liquidity into the cash strapped system.

Markets have been facing tight liquidity conditions for a while. In fact, liquidity deficit widened after companies completed their advance tax payments on December 15, 2011.

In order to boost liquidity, RBI started buying bonds by conducting OMO since the middle of November and till December end had purchased Rs 412.1 billion worth of government securities.

So far OMO has received good response from the market participants, and continuation of the same has supported bond prices a great deal.

After witnessing almost a secular uptrend for a large part of the month, government bond prices lost their way towards the end.

Encouraging economic data from US and Germany eased concerns over global economic growth, thus improving risk appetite globally. This made domestic bonds less attractive and led to the fall in their prices.

Sentiment was also hit as slowdown in the economy and poor tax collections raised fear that fiscal deficit for the year may overshoot the targeted 4.5% of the GDP by a huge margin, which may in turn imply a further increase in market borrowing.

This coupled with sharp rise in fiscal and revenue deficits during Apr-Nov converted the market’s worst nightmare in the recent times--further increase in borrowing--into reality.

On the last day of the year, after market hours, the RBI said that the government will borrow Rs 400 billion over and above Rs 4.7 trillion targeted for the year. As expected, market sentiment was severely dented and bond yields zoomed.

Given the present scenario, the last quarter of FY 2011-12 promises to be a frenzied one for bond markets in terms of supply.