Goals-based financial planning is here to stay, and for good reason. Using a goals-based framework in financial planning led to an increase in investor wealth of more than 15%, according to research by David Blanchett, Morningstar’s head of retirement research. Beyond returns, investors get a sense of motivation and satisfaction with their financial plans when advisors focus on a client’s personal goals versus arbitrary benchmarks.

But for goals-based planning to succeed, investors need goals that are important and achievable. Just asking investors what their goals are isn’t the solution. Investors might respond with answers that are seemingly reasonable, but research indicates many of these on-the-spot statements reflect top-of-mind priorities that might not represent the goals that are truly important to them.

These thinking blind spots can stem from behavioural biases we all share, and biases can wreak havoc on the best-laid goals-based plans. These blind spots can prevent investors from reporting their true goals and lead to financial plans that don’t accurately represent their preferences and motivations.

These blind spots are obviously a huge barrier to successful planning, so we conducted an experiment to see if a simple behavioural nudge – a master list of common goals – could help investors better identify what’s really important to them.

Our results suggest that there’s indeed a gap between the goals investors initially think they want and the goals that are truly relevant and important to them. This nudge can help investors find deeper insight into their overarching long-term aspirations and in doing so improve their chances of success.

Blind Spots are the goal-killers

Everyone has behavioural biases, and some of these biases pop up when we look for financial goals because of the emotions involved, the complexities of the decision, and the difficulty of forecasting our future desires. Many investors rely on mental shortcuts, such as the availability heuristic – focusing on readily available information when making judgments about what’s important.

For example, an investor who recently attended a housewarming party might say that her top financial goal is to buy a house, simply because that’s top of mind and easy to remember. Such mental shortcuts can overlook other financial goals that may actually have greater importance. Research suggests that without proper guidance, individuals often fail to identify as many as half of the goals that they later recognise to be central to their plans.

In a moment, these knee-jerk goals may not paint the full picture of a financial life that really is important to the person.

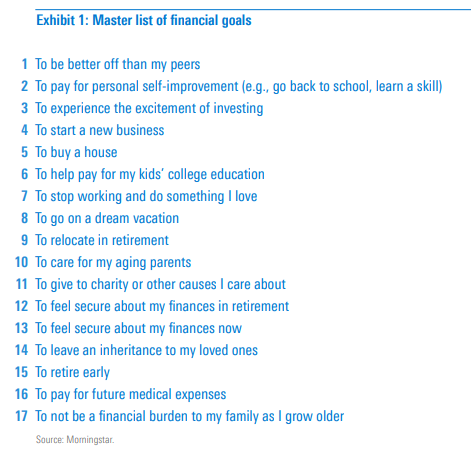

To prompt more-thoughtful goal identification, past research suggests that a carefully curated list – a master list – of common objectives can be effective. Master lists have been shown to improve preference identification across a variety of areas.

Our research tested the effectiveness of lists for identifying financial goals. We wanted the answer to the question: How can we help investors identify their true financial goals, and not only those that are top of mind?

Overcoming Blind Spots

To mimic the typical goal-identification process, we asked research participants to list and rank their top three financial goals. We then added their self-reported goals, in a random order, to a master list of common financial goals, creating a combined list. After viewing this combined list, participants were then asked to rank all the financial goals in order of importance.

To analyse the data, we mapped self-reported goals to those already on the master list and grouped similar self-reported goals together. This process helped us pinpoint only goals that changed substantially after seeing the master list.

If the master list had no impact on goal identification, then we would expect people to choose the same top goals that they self-reported compared with the goals they identified after seeing the master list. That wasn’t the case.

On average, 26% of participants changed their top goal after seeing the master list. The master list was even more impactful in a multiple-goal scenario: About 73% of participants substituted at least one of their top three goals with goals from the master list.

That means only about 26% of participants retained all of their top three initial financial goals, and this highlights a flaw in the traditional goal-setting approach used by financial professionals.

How did the goals change?

Once we discovered that the master list had a significant impact on investment goal priorities, the next question we asked was, “What happened?” What changes did the master list trigger?

We found that many people seemed to prioritise goals that were more personalised, detailed, and emotionally grounded after viewing the master list, and the use of a master list also seemed to nudge investors toward more-specific goals.

Retirement: Still King

Consistent with previous research, we found that “retirement” was the top financial goal. It was ranked as the top goal two and a half times more often than any other goal, with the residual category “others” and “financial security” trailing far behind. For many investors, retirement is a necessary focus, especially given the looming retirement crisis.

Given the impact of the master list intervention, a notable concern is steering investors away from objectively important goals, such as retirement, but our results suggest that the master list didn’t seem to have this effect. Among those who initially self-reported retirement as a top priority goal, only 16% changed it after seeing the master list. Those who were impacted by the master list commonly moved toward emotionally based goals. The next two sections provide insight into how people’s goals changed after seeing the master list.

Sharpened focus

In cases where investors changed their top goal, 27% made it more specific. For example, investors who previously listed “grow wealth” as the top goal swapped it out for goals that better encapsulated their motivations, such as achieving financial security or increasing social status. Many investors tend to think of goals as overarching milestones that won’t be reached for years – which leads them to set goals that might be too broad or vague.

But clear, detailed financial goals resonated with investors. So, the use of a master list seemed to help investors reflect on the underlying intent of their initial goals, leading them to better-refined priorities. Emotions matter We found that about half of the people who changed their top goal focused on emotions instead of outcome. Using a master list drew an important parallel between emotional returns and financial returns.

Many people who changed their goals settled on outcomes that revolved around emotional security, such as “to feel secure about my finances now” and “to not be a financial burden to my family as I grow older.” While emotions are often seen as anathema to sound financial decisions, our results suggest that there’s a big emotional component to holistically defining financial goals.

The list is the thing

Behavioural science shows that people can sometimes be strangers to themselves. Many investors are attracted to the level of personalisation of goals-based planning, and this approach is more popular every day, but it hinges on investors really knowing their investment goals and being able to communicate them clearly. This may be a lot more difficult than just straight-up asking clients to identify their major goals off the top of their heads.

Helping investors make good choices and develop plans that make long-term objectives possible should be one of a financial planner’s key missions, and our research found that master-list nudges might help guide investors toward the goals they really want.

Our experiment found that:

Master lists may help investors identify their goals: The majority of people we studied changed one of their self-selected goals after considering the master list, so we see clear benefits for advisors when they use a master list to identify and discuss goals with clients during onboarding and discovery

Master lists may help investors refine and focus their goals: People’s self-reported goals were often vague in our experiment, and that’s a recipe for disengagement. The introduction of a master list seemed to help people understand the underlying purpose of their goals, and this led to them adjusting their goals to ones that were clearer and more precise.

Master lists may help investors uncover meaningful emotional connections to their goals: We found that many investors updated their goals to ones that were both sensible and aligned with emotionally driven motivations after viewing the master list. This showed that viewing the master list might have stirred up personal connections to goals that they might not have realised when they listed goals off the top of their heads.

This post initially appeared on Morningstar.co.uk