This post by Saurabh Mukherjea was originally published on CFA Institute's Enterprising Investor.

When it comes to earnings growth, the Nifty 50 has not only trailed the larger Indian economy over the last decade, it has also lagged behind the S&P 500 by a country mile. Yet India’s economic growth is vastly outpacing that of the U.S. This bizarre phenomenon has far-reaching implications for Indian investors.

India’s GDP growth has averaged 13% per year in nominal terms since 2009, while NIFTY 50 earnings expanded at 8% annually on average. In fact, in 9 of the last 10 years, NIFTY 50 earnings growth has trailed that of nominal GDP by a wide margin.

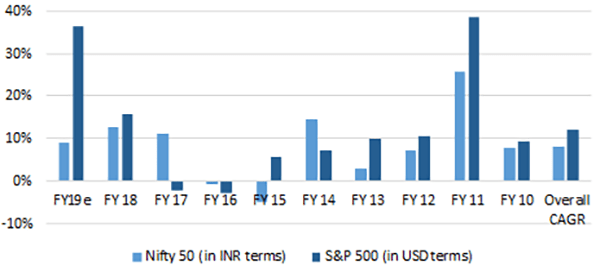

In the U.S., on the other hand, nominal GDP growth over the past decade has hovered at barely 4%. Nevertheless, S&P 500 earnings have grown at 12% annually. That’s a full 400 bps faster than the NIFTY 50 — and that’s without converting NIFTY 50 earnings into USD!

Which begs the question: Why do the benchmark indices in India and the U.S. display completely opposite trends relative to GDP growth?

Why does the NIFTY 50 lag the Indian economy?

To understand why the NIFTY 50 no longer captures the dynamism of the Indian economy, a good place to start is the index as it stood in 2009.

On the face of it, the 10-year share price return from investing in the index is a respectable 14%. But that figure is deceptively flattering. The NIFTY 50’s quality — or lack thereof — is reflected in returns from the 50 stocks that composed the index in 2009. Such an equal-weighted portfolio would yield an annual return of -1% (CAGR over 10 years). And, again, that’s after beginning the measurement period in February 2009, when the market was close to its post-Lehman Brothers nadir.

If the typical investor’s cost of equity in Indian stocks is 15%, only 19 constituents of the NIFTY 50 delivered returns in excess of that. And that figure is also enhanced by the February 2009 start. These 19 outperformers — ranked in descending order of performance — are HCL Tech, TCS, HDFC Bank, Maruti Suzuki, M&M, Zee, HUL, HDFC, Wipro, Tata Motors, BPCL, Infosys, ITC, Siemens, Hindalco, ICICI Bank, Grasim, L&T, and Sun Pharma. With four exceptions, all of these firms are from such relatively capital-light or business-to-consumer sectors as consumer, auto, pharma, and banking.

The other 31 companies whose 10-year returns are below the cost of capital are from balance-sheet heavy sectors: power, construction, metals, telecom, real estate, and oil and gas. Together, these accounted for roughly 30%–35% of the Indian economy, according to government data. And yet these companies made up two-thirds of the companies in the NIFTY 50. That leaves little room in the index for firms that represent more vibrant sectors of the economy.

The over-representation of capital-heavy sectors explains much of the NIFTY 50’s sluggish performance.

Why the NIFTY 50 continues to have such a high proportion of companies from balance-sheet heavy sectors is not immediately obviously.

Moreover, over the last five years, the NIFTY 50’s performance has increasingly diverged from that of India’s nominal GDP, after faithfully tracking it for much of the preceding decade. This suggests many of the drivers of the Indian economy are no longer in the listed market. For example, taxi aggregators, like Ola and Uber; online retailers like Flipkart and Amazon; electronics goods manufacturers; car manufacturers other than Maruti; hotels besides Taj, Oberoi, and Lemontree; etc., are all unlisted.

Most of what affluent India buys no longer appears in the listed market either. The companies that cater to the wealthy can access capital at low cost without entering the stock market, so their contribution to GDP is not reflected in any index. If, as the Indian economy matures, the unlisted world continues to provide capital at lower cost than the listed market, then the gap between GDP and market cap will widen further.

What are the implications for investors?

- The NIFTY 50’s sluggishness makes it easy to outperform. While that makes the plight of NIFTY 50 tracker/index funds a difficult one, it also opens up enormous opportunities for Indian smart beta funds. For example, the NIFTY Junior, which represents the 50 most liquid stocks below the NIFTY 50, almost always outperforms.

- Since two-thirds of NIFTY 50 constituents have failed to generate returns that exceed the cost of capital, large-cap Indian funds composed of mostly NIFTY 50 stocks are difficult investment to justify. On the other hand, even a relatively simple strategy — like our Consistent Compounders algorithm, which focuses on a select subset of NIFTY 50 stocks — can deliver returns that consistently exceed the cost of capital.

- The Indian stock market’s failure to provide lower-cost funding than private equity firms is depriving the NIFTY 50 of high-quality companies that can better align the index with the larger Indian economy. The more critical foreign and private equity-funded firms become in India, the bigger the questions mark around the relevance of the Indian stock market as a medium through which ordinary investors can benefit from the country’s economic growth.

- That S&P 500 earnings outpace U.S. economic growth suggests that US companies can tap into emerging markets much more effectively than NIFTY 50 firms. This raises troubling questions about the quality of capital allocation and accounting in NIFTY 50 companies and suggests that Indian investors should perhaps consider a diverse portfolio of global companies.

- There is a widespread misperception that by building portfolios that overweight to small and mid caps, investors can beat the NIFTY 50’s slow earnings growth. But such a strategy, like buying small-cap exchange-traded funds (ETFs), does not protect investors from the underlying challenge: That private equity can cherry pick the best opportunities while the capital markets are dominated by sclerotic sectors and the dregs of the Indian economy.