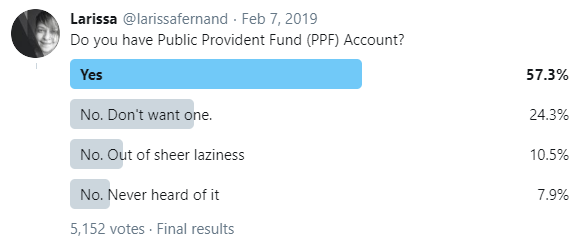

Last year, I conducted a Twitter poll and was pleasantly surprised with the response. But the outcome took me aback. I was unaware as to how many did not have a Public Provident Fund (PPF) account. If you don't, I suggest you read How to get the best out of a PPF account.

I, for one, would always encourage individuals to open a PPF account. While I am still a big fan, my perception over the years has changed. Let me explain why.

The mistake I always made when I suggested PPF was simply viewing it as a great debt product which is high on safety and super tax benefits. Think about it, putting away money for 15 years with a guaranteed return that is tax free and risk free. Who would not want to opt for it?

But being a great product does not imply that it is a natural fit in any portfolio. Does it find a strategic place in your portfolio? Does it fit in with your financial plan?

Maybe it does…

A financial adviser told me that the equity allocation in his personal portfolio is done via systematic investment plans (SIPs) in equity mutual funds and direct purchases of stocks. Interestingly, when it comes to the debt allocation, he invests Rs 1,50,000 every April in PPF and the balance debt allocation will go either into debt funds or balanced funds.

In my case, the PPF is part of my overall debt allocation. I invest in non-convertible debentures, credit funds, fixed deposits and debt funds. The assuredness of return, the safety and longevity of PPF appeals to me.

A family member has a PPF account and so does her husband. They both contribute Rs 1,50,000 each, every year, into their own respective accounts. They have plans to extend it for the 5-year blocks on maturity, so eventually it will form part of their retirement kitty. This along with their EPF forms part of their debt allocation.

For some it does not…

A consultant told me that the PPF did not make sense for him from a practical standpoint. He was not assured of a monthly steady income, and so cash flow fluctuated. As a result, he was just not comfortable locking up money for an extremely long duration which could not be easily accessed.

Also, salaried individuals who are contributing to the Employee Provident Fund (EPF) and Voluntary Provident Fund (VPF), could bypass the PPF. For the EPF, a salaried individual will contribute 12% of his Basic + Dearness Allowance and the employer will match the contribution. The employee can also opt for VPF and top up the contribution to the provident fund, though the employer won’t match this. The returns too are marginally higher than PPF and the safety factor holds, as does the tax benefit.

Some of my colleagues tell me that they cover Section 80C with life insurance premiums, child’s education fees, contribution to EPF, and investments in Equity Linked Savings Schemes (ELSS). They do not feel the need to own a PPF account to form part of the debt allocation of their portfolio. If that confused you, do read Tax Saving: Earn the right to invest.

Interestingly, one of them was not in favour of PPF. His portfolio was heavily tilted towards equity since he had decades to retirement. And since equity gives a much better return, why channelize the money to an investment with such a long lock-in period?

Very pertinent point.

Many find the PPF tenure to be agonizingly long, a 15-year investment with a 16-year lock-in. The first year is not taken into consideration when looking at the maturity of the account. The end of the financial year in which the deposit was made is what matters. So if you opened the account on July 15, 2000, the 15-year tenure will commence from end of FY2000-01 (March 31, 2001). That means, it would have matured on March 31, 2016.

He later came to realize that the lock-in was a blessing of sorts. It just kept silently growing with no effort on his part. Even if he was low on cash, he could deposit just Rs 500 per annum to keep it going. He invests in it now, not for its tax benefit, but for the stability and safety it offers.

There is no one size fits all when it comes to investing. As Deepak Khemani of Khemanis always says: "It is personal finance, personalize it."