Cyber security is one of the foremost concerns of the Aerospace and Defense (A&D) industry. Combatting cyber threats to defense and civil infrastructures has become a global priority for governments. Not too long ago, a U.S. federal government website was hacked and Australia's government and institutions were being targeted by sophisticated state-based cyber hacks.

So it should come as no surprise that some U.S. defense contractors rank among the world’s top 25 cyber security companies.

A very recently published article noted that tech startups were oblivious to one of the largest markets in the world, the U.S. Defense Department. The military awarded $445 billion in contracts in 2020, when the global market for software-as-a-service, one of the hottest sectors for startup creation and investment, was estimated at $104 billion.

Why defense as a “sin stock” is defunct.

The concept of sin stocks has given way to viewing businesses that have a positive impact on three parameters – Environment, Social, Governance.

ESG attempts to capture the complexity of social and environmental systems, and business organizations. It is not narrow, where the fixation is on identifying the final output and classifying it as a sin stock. It goes beyond its 3-letter acronym to address how a company serves all stakeholders: employees, communities, customers, suppliers, shareholders, and the environment.

The A&D industry is a high-technology industry and covers a diverse set of companies providing products and services to civil and military customers. Stocks are evaluated on good company behaviour, rather than the narrow prism of purely controversial end products. I tackled this in Why sin stocks are an outdated concept.

In a July 2020 report, Sustainalytics listed a few parameters they consider when evaluating the ESG score of A&D firms.

ESG Risk Ratings indicate 5 levels of risk (Negligible / Low / Medium / High / Severe), rated on a spectrum of 0 to 40+. These take into account a company’s exposure to industry-specific ESG risks and how well a company is managing those risks.

The A&D industry is generally seen as high risk; 62% of companies considered high risk (ESG Risk Rating scores between 30 and 40), 21% considered severe risk (ESG Risk Rating scores above 40), primarily due to high exposure and mixed management.

Relatively high exposure to material ESG risk due to several factors, including its concentration in highly regulated markets and high degree of regulatory scrutiny.

This is among the highest in the entire research universe, as quality and safety regulations are extremely tight, and even minor defects can have significant impacts. More than two thirds of the industry (68%) has high exposure score (i.e. >8); 49% of companies show weak management scores (i.e. scores 50). The combination of high exposure and weak management means that 17% of the industry have severe unmanaged risk (i.e. scores >8).

A&D companies have medium exposure (i.e. scores between 4-8). The industry is potentially exposed to bribery and corruption due to its close business relationships with governments, its competition for a limited number of high-value contracts and secrecy surrounding military procurement.

As part of a heavily regulated industry with a global presence, A&D companies are subject to intense scrutiny on anti-competitive practices and ethical conduct related to products sold in sensitive areas. Exposure is medium for the subindustry as a whole, but tends to be higher for defense companies, which can be involved in weapons-related incidents.

- Carbon – Products and Services

The industry has medium exposure (i.e. scores between 4-8) to Carbon – Products and Services risks. These risks tend to be higher for aircraft and components producers, whose clients are energy intensive and operate in a tightening regulatory environment around the carbon impact of air travel. Despite the increasing visibility of carbon--related issues, the industry has not recently faced any related events.

- Data Privacy and Security

The industry’s exposure comes mainly from companies’ heavy reliance on sensitive data. A&D companies are among the largest government contractors and are entrusted with managing, storing and processing highly confidential information. The inherent secrecy of government contracts explains, in part, the low levels of company reporting on data privacy and security issues. Almost half (43%) of the companies in the industry have weak management scores (i.e. scores of 0-25). However, the increasing pressure to secure highly sensitive data from espionage is driving companies to improve their safeguards. Overall, more than half (60%) of the industry shows low unmanaged risk (i.e. scores of 2- 4) while 38% face medium risk (i.e. scores of 4-6).

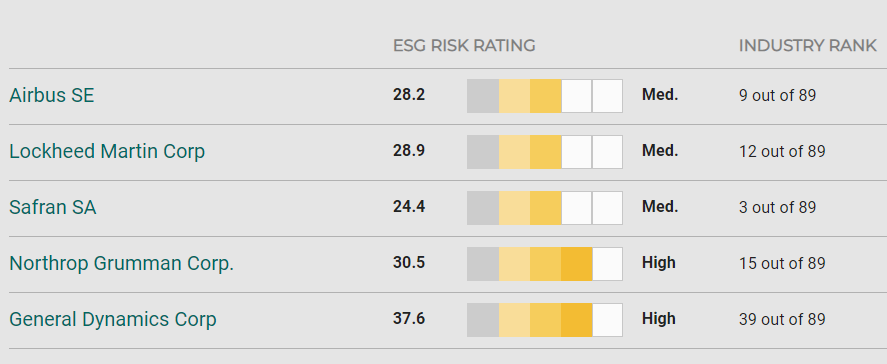

Here is an illustration of how some companies in the A&D industry are ranked by Sustainlytics, as on April 15, 2021.