This article has been co-authored by Dr. Nupur Pavan Bang, who is Senior Researcher, Centre For Investment, Indian School of Business, Hyderabad. An abridged version of this article was first published in Mint on February 21, 2013 and is available here. The full article is carried below.

Mutual fund investors seem to be a disgruntled lot these days. It would not be fair to paint everyone with the same brush, but the overwhelming feeling we get via various forums is that mutual fund investors (especially on the equity side) are quite dissatisfied with the performance of their funds.

Who’s to blame them really—after all the equity markets have pretty much not gone anywhere over the past five years, with the benchmark indices yielding flattish returns. For example, Sensex was around the 20,000 mark in the beginning of 2008, and it remains close to that mark, five years hence. Although there may be a time period bias here (of looking at a point-to-point period), there is no doubt that the patience of equity fund investors has truly been tested over the past five years, especially for those that have remained invested.

Retail Investors Have Typically Not Been Good Market-Timers

The time of entry also becomes a crucial factor in gauging the investor experience. After all, retail investors have historically not been good market-timers, whether in India or globally.

As renowned fund manager Prashant Jain of HDFC Asset Management points out in various forums, retail investors tend to usually enter the market in higher volumes in the last leg of the rally, when the markets have already moved up significantly and P/E multiples are higher.

Barber, Odean and Zheng (2003) in their research find that investors ‘over-optimistically’ bet on past returns as an indicator of future performance (representative heuristic) when they buy mutual funds. On the other hand when they sell, they tend to dispose of superior performers and continue to hold losing investments (disposition effect). Similarly, Fiotakis and Philippas (2004) find that in Greece, mutual fund investors are active trend chasers and their investment decisions are wrong and short-lived.

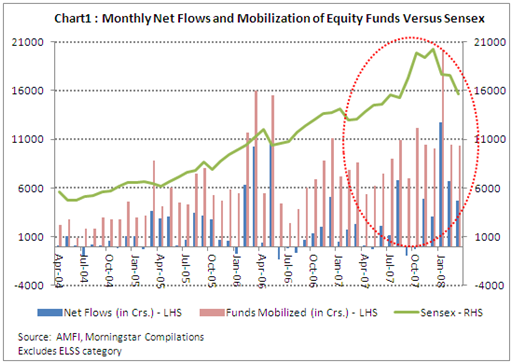

A look at equity fund flows and mobilization trends in Chart 1 and Table 1 support these arguments in the case of Indian individual investors too. In FY 04-05, equity funds registered a net inflow of only Rs. 7,293 crores, while the Sensex hovered between levels of 5,500 – 6,500 during the year, and was available at attractive valuations.

Flows picked up considerably in FY 05-06 and breached the Rs. 31,000 crores mark. The number of equity fund folios (which is an indicator of number of investors) also grew by more than 80% during the year. Over the next two financial years, the flows and mobilization of equity funds remained robust and continued to grow. During FY 07-08, the net inflows of equity funds were the highest at almost Rs. 41,000 crores, even as the Sensex climbed to a peak of around 21,000 in January 2008, before dropping to around 15,600 levels by the end of March 2008. The number of equity folios crossed a record 3-lakh mark, and grew by 46% during the financial year.

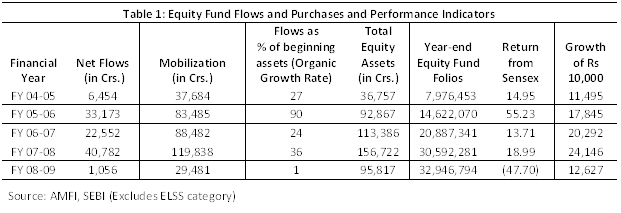

Despite the absolute quantum of inflows being the highest in FY 07-08, the organic growth rate (inflows as a percentage of beginning assets) was actually the highest at 90% in FY 05-06, when the Sensex was at much more attractive levels. This indicates that despite the relatively smaller size of the industry then, there were many investors who invested in FY 05-06, and would have benefited because they entered at the beginning of the rally. In FY 07-08 the organic growth rate was a healthy 36%, but considerably lower than that of FY 05-06. However, that doesn’t disguise the fact that investors continued to pour money into equity funds in FY 07-08 even as markets breached new highs, and elements of froth became more evident.

We can see from Table 1, that an investor who got in at the last leg of the rally would have lost about 48% in a single year, and hence this would have been quite disappointing, in spite of the funds claiming to have performed well in terms of total returns over a 5-year period. For the growth of the asset management industry, the investor experience is quite crucial, and that will also help to expand the acceptance of mutual funds, especially among retail investors. A good barometer for measuring investor experience is “Investor Return”.

What is Investor Return?

Investors often tend to suffer from poor market timing and planning, as highlighted above. A fund’s total return reflects a buy-and-hold strategy. But in reality you have different investors subscribing or redeeming from the fund at different points of time. So the actual return earned by an investor may be quite different from the total return that the fund displays.

Investor Return, according to Morningstar’s definition, "measures how the average investor fared in a fund over a period of time. Investor return incorporates the impact of cash inflows and outflows from purchases and sales and the growth in fund assets". It takes into account the fact that not all investors would invest and redeem at the same time. Hence it places a higher weight to returns when assets invested are higher and lower weight to returns when assets invested into funds are lower. As with an internal rate of return (IRR) calculation, investor return is the constant monthly rate of return that makes the beginning assets equal to the ending assets with all monthly cash flows accounted for.

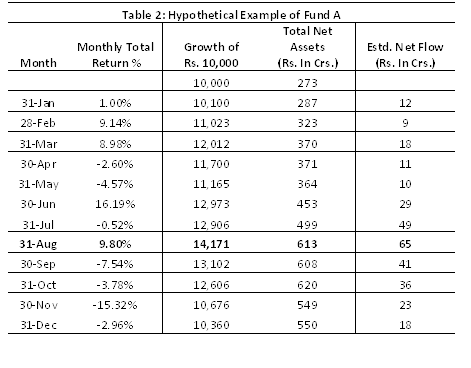

Let's explain this with the help of a hypothetical example:

Fund A’s assets grew rapidly to Rs. 613 crores in August. Until then an initial investment of Rs. 10,000 in the fund had grown to Rs. 14,171. However, post August the fund started generating negative returns. Also, around 57% of the fund’s overall inflows for the year came in between August and December. Investors who purchased the fund in August clearly did not have the same experience as investors who bought the fund in January. Investors who bought the fund in January and remained invested made a total return of 3.60%. In contrast to total return, the investor return (or what the average investor earned) over this time period is -10.98%.

Minding the Gap is Important

Investor return is not a substitute for total returns, but can be used in combination with total return. The gap between investor return and total return indicates how well investors timed their fund purchases and sales. When investor return is less than total return, it means that investors didn’t participate equally in the fund’s monthly returns—more investors participated in the downside returns and less in the upside returns. This sometimes happens when investors chase returns and assets flow into a fund at its peak of performance.

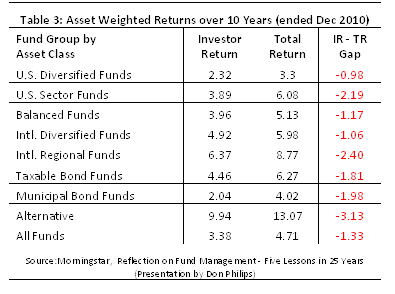

To see how investors have fared in the United States, Morningstar calculated asset-weighted investor returns for fund asset class groups over the past 10 years (ended December 2010) and then compared it with the category averages. A behavior gap seems to be evident in all fund asset classes as per Table 3 highlighted below.

According to Morningstar, “In addition to revealing patterns of investor behavior, investor returns can also shed light on how well fund families are preserving the investor experience. It is the responsibility of fund companies to promote sound investment strategies. If the fund companies are encouraging short-term trading and trendy funds, they may not be looking at investor’s long term interests. These fund companies are likely to have funds with low investor returns relative to total returns.”

Therefore, minding the gap over the long term is quite crucial. After all, the investor experience is paramount, to repose faith in equity-investing again.