Fund sizes have grown tremendously over the years. For instance, the largest actively managed fund Kotak Flexi Cap Fund manages assets worth Rs 32,453 crore.

The growing size of funds has often raised concern among investors about the fund’s ability to sustain performance. The new categorisation norms which define where fund managers can and cannot invest has raised the bar further for fund managers.

Pros and cons of small versus big size

The biggest edge small funds have is the agility to move in and out of stocks swiftly. A fund size with Rs 30,000 crore assets under management, or AUM, will have to sell stocks worth Rs 300 crore to offload 1% of holdings in a stock which could take a few days or a week, depending on the liquidity. Similarly, a fund with Rs 300 crore assets has to sell just Rs 3 crore worth of stocks to offload 1% stake. Thus, a small size indeed gives the agility for a portfolio manager to move in and out of stocks swiftly, thereby capitalising on certain events.

A fund with a small AUM has certain disadvantages as well. For instance, if a few investors hold a sizeable portion of assets their exit can hurt the performance of the fund.

Sandeep Tandon, CEO, quant AMC, says, “The biggest disadvantage is that we cannot participate in Initial Public Offerings or IPOs/Blocks neither as an anchor investor nor as a normal investor due to small allocations. Further, corporate access is very limited which means that we have to largely rely on our in-house research and analysis.”

On the other hand, funds with large AUM have enough cash holdings to meet redemption pressures. The exit of a few large investors would not have a meaningful impact on the fund. Since the fund house earns decent revenue from a large fund, it could deploy more resources and strengthen the research which would ultimately benefit investors. Further, economies of scale resulting from large size are passed on to investors in terms of lower Total Expense Ratio or TER.

Drivers of performance

A fund’s performance is driven by multiple factors like investment mandate, style, ability to stick to one’s conviction, processes and research capability of a fund house, consistent inflows in schemes, macro/micro factors and so on. The fund’s size is a reflection of the fund’s popularity among investors and the AMC’s ability to sell it.

Investors tend to chase performance. If a fund has grown too big in size, it must be due to the fund’s ability to generate superior risk-adjusted return in the past.

“It’s a myth that portfolio size affects the performance of a fund. Rather, performance can be explained by the investing style. At quant, we practice a very dynamic style of money management that entails actively updating the portfolio based on prevailing market conditions,” adds Sandeep.

Size becomes relevant in funds that have a fixed mandate to invest in a particular market cap, for instance, mid cap and small caps. Kaustubh Belapurkar, Director – Manager Research, Morningstar Investment Advisers, says that the size of the fund needs to be looked at from the context of the investment mandate of the fund. “The current AUM should allow for an adequate investable opportunity set to continue to manage the fund as per the investment mandate. For certain types of funds a large AUM can be challenging e.g. mid and small cap funds where the opportunity set may be limited and increasing AUM may result in over-owning the same stock (i.e. owning a greater share of the company’s equity) which can also result in poorer liquidity of the portfolio.”

Due to such challenges, a few small cap funds stop accepting fresh inflows or lumpsum investments if the fund’s size becomes unmanageable.

Mumbai-based RIA Suresh Sadagopan does not use fund size as a filter while choosing funds. “We expect the fund manager to find appropriate opportunities for investing including ensuring liquidity.”

We pulled out data from Morningstar Direct to ascertain how large sized funds have performed vis-à-vis their smaller peers.

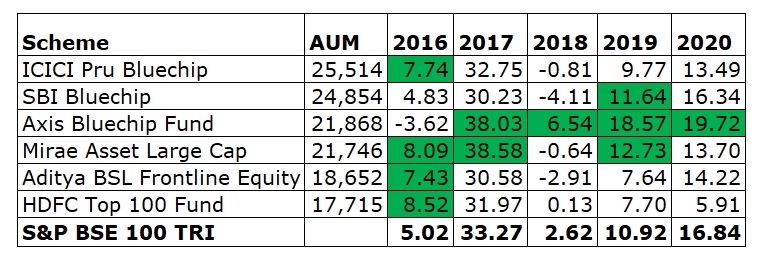

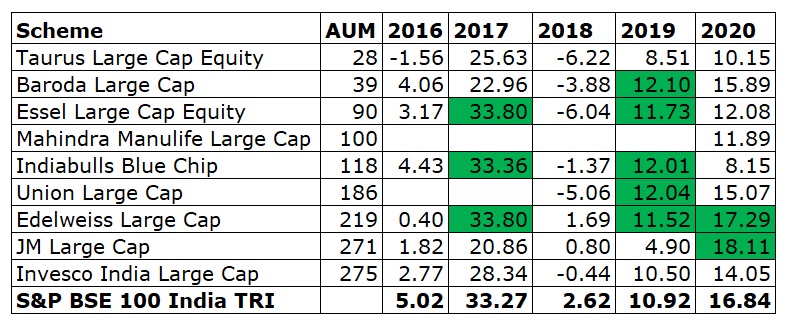

Large Cap

In calendar year 2020, the S&P BSE 100 delivered 16.84% return. During the same period, only six funds were able to beat this benchmark.

HDFC Top 100 Fund, the sixth largest fund in the category, delivered 5.91% in CY 2020. If we compare HDFC Top 100 Fund’s performance with ICICI Prudential Bluechip, the latter has outperformed by 7.58 percentage points despite being the largest fund in the category. But HDFC Top 100 Fund has not necessarily underperformed merely due to its size. The fund manager had exposure to PSU stocks which hurt the fund’s performance in the past. On a YTD basis, HDFC Top 100 Fund has performed well (12.46%) on the back of broad-based rally in the market and the value stocks in the portfolio performing well.

Performance large cap (largest funds)

(Funds with AUM exceeding Rs 15,000 crore were considered)

Performance large cap (smallest funds)

(Funds with below AUM Rs 300 crore were considered)

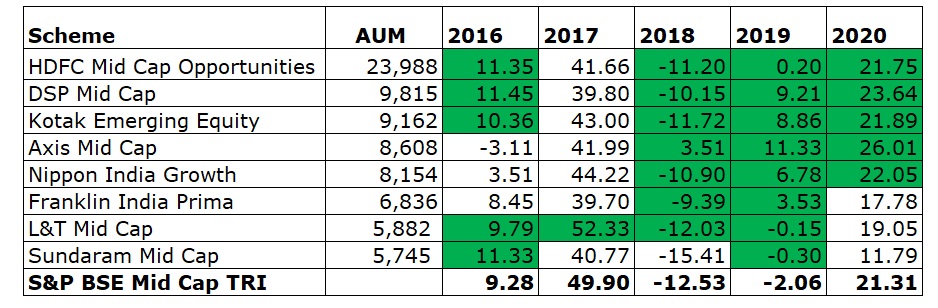

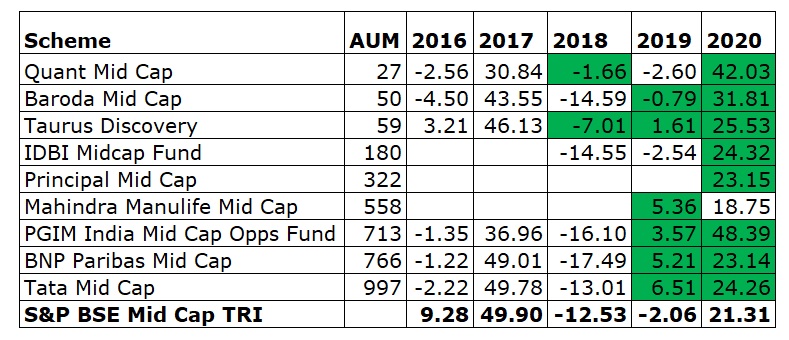

Mid Cap

In CY2020, the S&P BSE Mid Cap delivered 21.31% return. Of 28 funds in this category, 18 funds outperformed the benchmark.

PGIM India Midcap Opportunities Fund, which ranks 20th in the AUM pecking order, with asset size of Rs 713 crore has topped the performance chart. It delivered 48.39% return in CY 2020, outperforming the benchmark by 27.08 percentage points.

The five largest funds (with AUM in excess of Rs 8,000 crore) delivered an average return of 23.07% return in CY 2020. The five smallest funds (AUM less than Rs 200 crore) delivered an average of 29.37% return in CY2020. This shows that small sized funds have outperformed the large peers by 6.30 percentage points.

The BSE Mid Cap dipped by -2.06% in CY 2019 while Axis Mid Cap Fund (which had AUM of Rs 4,140 crore in December 2019) delivered the highest return at 11.33%. Other large sized funds like DSP Mid Cap, Kotak Emerging Equity and Nippon India Growth Fund outperformed the benchmark index by a wide margin in CY 2019 even as the Mid Cap Index was in red. Thus, one cannot conclude that size is the only determinant of performance since large sized funds were able to not only protect the downside but generate a positive alpha in CY 2019.

“If the fund’s sectoral skew is more towards businesses which are in the low cycle and will take time to recover, that will have a bearing on performance. It also depends on the overall valuation paradigm on which the investment opportunities are available. There will be lesser investment opportunities at higher valuations and this will also impact the performance of the fund,” says Vinit Sambre, Head of Equities, DSP Mutual Fund.

Performance of mid cap (largest funds)

(Funds with AUM above Rs 5,000 crore were considered)

Performance of mid cap (smallest funds)

(Funds with AUM below Rs 1,000 crore were considered)

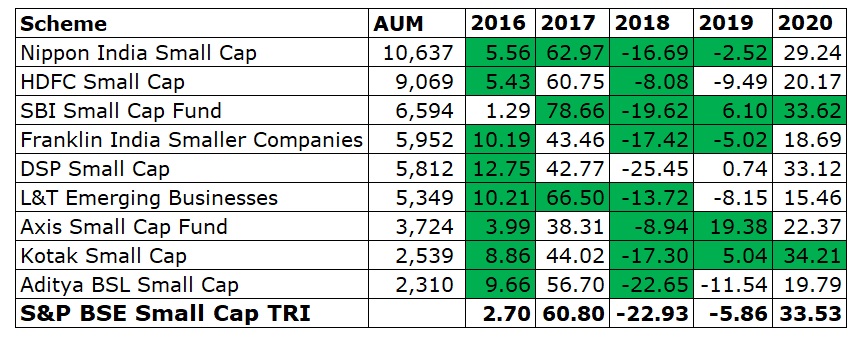

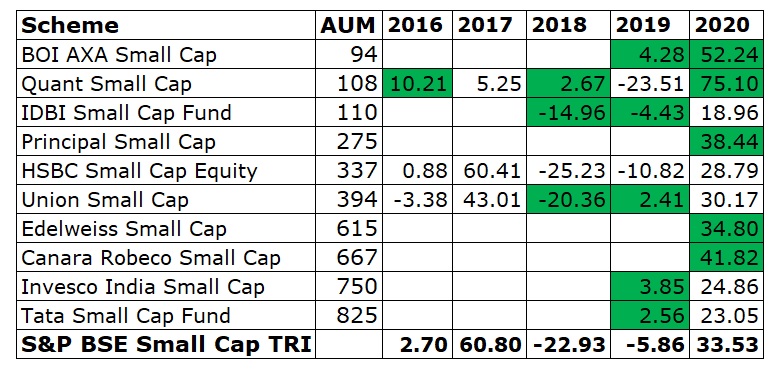

Small cap

Of 21 small cap funds, only seven funds outperformed the S&P BSE Small Cap Index in CY2020. Of the seven funds which outperformed, five funds had AUM below Rs 700 crore. SBI Small Cap, with AUM of Rs 6,594 crore, was the only fund among the large sized funds, which outperformed the index.

The five smallest funds with AUM less than Rs 300 crore, delivered an average of 46.19% in CY2020. On the other hand, five funds with AUM exceeding Rs 5,000 crore each, delivered an average of 26.97% during the same period.

This implies that small sized funds have delivered better returns than their large peers. However, selecting funds merely based on AUM criteria, even in small cap category, could backfire. In CY2019, the Small Cap Index fell by -5.86%. During this period, Axis Small Cap Fund had delivered 19.38% (highest) even as the small cap index was in red. Axis Small Cap had AUM of Rs 1,542 crore in December 2019.

In CY2019, quant Small Cap Fund delivered negative -23.51%. Thus, the small AUM size of quant Small Cap Fund did not help the fund in 2019.

Performance of small cap (largest funds)

(Funds with AUM above Rs 2,000 crore were considered)

Performance of small cap (smallest funds)

(Funds with AUM below Rs 1,000 crore were considered)

Summing up

Size brings in executional advantage in certain categories of funds, but it could be only up to an extent. Investors should consider the skill sets of a fund manager, fund house pedigree, the team, past track record and the processes of a fund house while shortlisting funds. While selecting funds in the mid and small cap space, it is advisable to go for funds that are neither too big nor too small. Size should ideally not be the sole criteria while choosing funds, especially in flexi cap, large cap or fixed income funds.

- Calendar year returns in %

- Green cells indicate these funds have outperformed the benchmark

- AUM Rs. crore as on January, 2021

- Funds that have not completed 1 year were excluded

- Blank cells indicate that these funds were not in existence during that period