A combination of factors like breakthrough in vaccination for Coronavirus, rising inflation, economic recovery and improving risk appetite have raised bond yields globally and in India. From 5.89% in December 2020, the 10-year government bond yield has risen to 6.13% in April 2020. Similarly, the U.S. 10-year treasury yield had risen to 14-month high of 1.76% on March 30, 2021.

The rising bond yields drive the prices of bonds lower, thereby negatively impacting debt fund returns. A hike in rates will impact the long duration bond funds the most.

The central bank had been lowering the interest rates to spur economic growth. Going forward, the expectation is that the Reserve Bank of India, or RBI, will roll back the liquidity measures and possibly hike rates once the economy picks up steam. However, the RBI monetary policy announced today kept the repo and reverse repo rates unchanged.

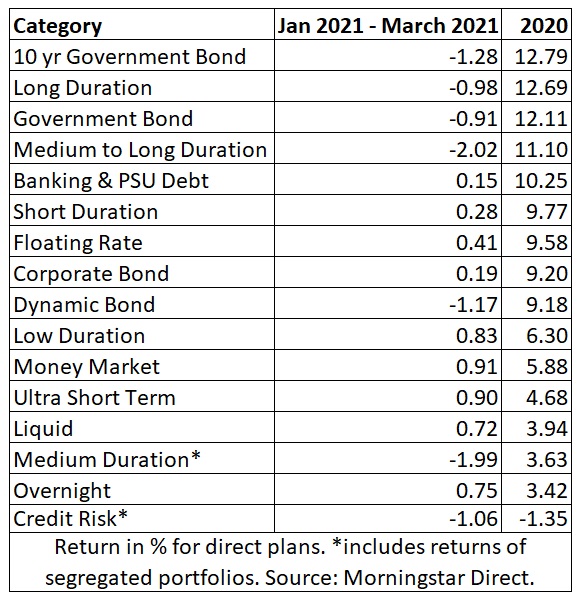

Here’s a look at the returns over calendar year 2020, and the first quarter of 2021 (January 1 – March 31). Over the last three months, constant maturity gilt funds, which invest in 10-year G-Secs, have yielded negative -1.28%. Last year, this very same category delivered 12.79%.

Investors have been moving to the shorter end of the yield curve. In February 2021, categories like low duration, money market and liquid funds received the bulk of the inflows worth Rs 29,725 crore. As interest rates went southward, long duration and gilt funds gained the most by delivering double digit returns. Will the party continue in 2021? Unlikely, say fund managers.

We asked debt fund managers about how they are navigating their portfolios at a time when bond yields are rising and share their advice for investors.

Reduced duration

We have started witnessing RBI unwind liquidity which started with variable reverse repo auction. They will also roll back Cash Reserve Ratio, or CRR. It will be done in a gradual and non-destructive manner because while growth is coming back the central bank is concerned that it is not on a strong footing. Even if it happens over nine to twelve months, there would be upward pressure on rates. With that in mind, we have reduced duration. We have come down below 4 years of Macaulay duration in SBI Magnum Income Fund at this point in time. We are trying to minimise the capital loss as the RBI unwinds liquidity.

We don’t expect RBI to hike the repo rate. But there is a possibility that RBI might narrow down the corridor between repo and reverse repo. This would put pressure on the short end of the curve while the longer end would also face pressure. We will see a flattening of the curve (narrowing of yield spread between short- and long-term interest rates) over the next six to twelve months as the liquidity is sucked out by RBI.

In medium to long duration funds, investors need to invest for a three to five years time horizon. Investors should have the discipline of staying invested even if they face some losses in debt fund in short term to get reasonable returns over the long run. – Dinesh Ahuja, Senior Fund Manager, SBI Mutual Fund.

Adopted a barbell positioning

Short term money market rate is 3.30%. The five-year government security yield is 6%, which is a gap of 300 basis point. We had been advising clients to stay away from long duration products. Investors should also avoid taking high credit risk at this juncture. Lower duration and good credit quality are preferred. Our portfolio is tilted towards government securities. We have higher cash with barbell positioning. (Half of the holdings are short-term instruments and the other half are long-term holdings). Thus, the combined duration is on the lower side.

Investors should acknowledge that the best of the bond market rally is now behind us and they should lower their return expectation from fixed income products. It would be prudent for investors to be conservative in their fixed income allocation. If you have a short investment horizon with low risk appetite, invest in liquid and overnight funds. If you have a slightly longer horizon and comfortable with volatility, you can look at short term categories or dynamic bond funds.

If you have invested in duration funds, try to have a holding period higher than the duration of the fund. If you have invested in your long-term retirement portfolio, do not make any changes to the portfolio as opportunities will be there across the cycle. Tax plays an important role. Before switching, consider tax implications. - Pankaj Pathak, Fund Manager, Quantum Mutual Fund.

Where should you invest?

Interest rate risk is prominent at this juncture as RBI will normalise liquidity at the end of the year. We need to see how the growth pans out this year. Average inflation will be lower this year as compared to last year but it would still be more than 4%.

With the economy improving this year, we are seeing improving credit environment. The credit ratio (ratio of upgrades to downgrades) which had fallen in the first half of calendar 2020 has improved sharply.

Investors should look at the duration of the fund and their time horizon while investing. They should not look at the past returns while shortlisting funds. There could be volatility in the next 12 months. To ride this volatility, investors should look at short to medium duration products. The curve is already very steep. Through short duration funds, investors can capture that steepness at the same time not take undue duration risk. – Anil Bamboli, Senior Fund Manager, HDFC Mutual Fund.

Watch this video to understand how to invest in a low interest rate scenario.