The oil shock continues. Brent crude briefly pushed over $110 per barrel Monday, with the war on Iran potentially creating extended disruptions to oil, gas, and naphtha supplies, Asian stock markets are reacting negatively to the risks of higher energy costs, with Japanese, Korean, and Taiwanese equities hit the hardest.

Why it Matters: The major risk impacting all countries is the short-term rise in fuel costs. There is a tangible reduction in the flow of oil and LNG through the Strait of Hormuz, but much of the jump in oil prices reflects rising risk premiums.

- Higher costs of goods will lead to pressure on consumer sentiment across Asia, which could impact 2026 demand. A prolonged rise in input costs may also defer company expansion plans. This includes delays in data center investment.

- Besides oil and gas, the Gulf region is a key supplier of naphtha to Asia. For example, 60% of Japan’s naphtha imports are from the Gulf. Countries may be able to rely on other feedstock in the short term, but costs will rise for petrochemical products, and this will weigh on a variety of consumer and industrial goods.

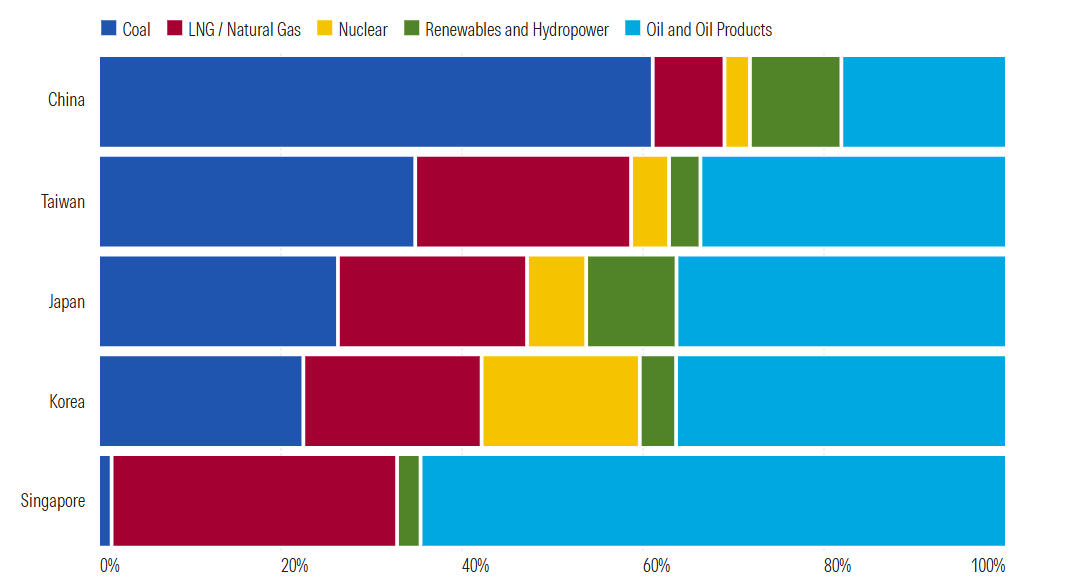

Energy Supply Mix by Country

Direct and as feedstock to other energy products

Source: IEA, Data for China, Taiwan, and Singapore as of 2023, and Japan and Korea as of 2024. Data as of March 9, 2026. Download CSV.

The Bottom Line: The uncertain outlook is hurting risk appetite, and we are seeing a flight to quality and cash. We think the impact on company earnings will be fundamentally limited over the medium and long term, and we will keep our valuations unchanged. We think some companies' share price drops already reflect the potential negative impact on near-term earnings.

- Notably, until Friday, March 6, outside of South Korea, Asian markets saw largely limited reaction to the war, not dissimilar to the average reaction to the outbreak of the Ukraine War. The sharp jump in oil prices on March 9 spurred more significant responses.

- We think other factors prior to this war, such as the selloff in software services companies, had already taken some money off markets. We think the disruption from the adoption of artificial intelligence will have a larger fundamental impact on select companies.

- With our valuations unchanged, we see sharper share price declines as potential buying opportunities. We prefer companies that we think were indiscriminately sold on the AI threat, such as Nintendo and Tencent. That share selloff is not enough to lead us to buy the broad market.

- We continue to see Korea as expensive, largely because of Samsung and SK Hynix, which have around a 40% weighting in its index. We currently rate both companies 2 stars.

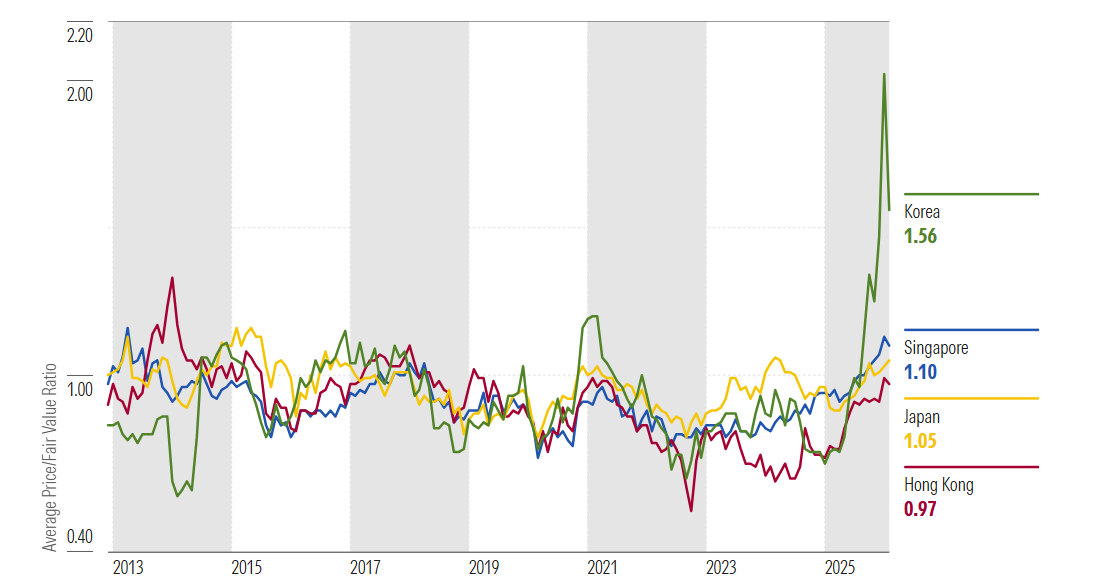

Price/Fair Value Ratios for Asian Markets

Average P/FV for each market over time leading up to the Iran war.

Source: Morningstar Investment Research. Data as of Feb. 28, 2026. Download CSV.

The Bear Case for the Iran War

A prolonged conflict will lead to financial stress and rolling blackouts that impede production, and possibly a global economic recession. This is not our base case, as we think the key Asian manufacturing bases have options that can be deployed to withstand short-term pressures.

- China, Japan, South Korea, Taiwan, and Singapore are net importers of energy with various exposures to supplies from the Gulf. We think the more immediate risk is to LNG supply from Qatar and naphtha from Saudi Arabia and the United Arab Emirates. Alternative delivery routes from Saudi Arabia may be possible and the countries do have strategic reserves to tap.

- Japan has 250 days’ worth of strategic oil reserves, while South Korea has 205 days’ worth. Taiwan has 100 days. China and Singapore have not publicly revealed the size of their reserves, but a past Reuters report estimates China’s to be at around 90 days of import needs.

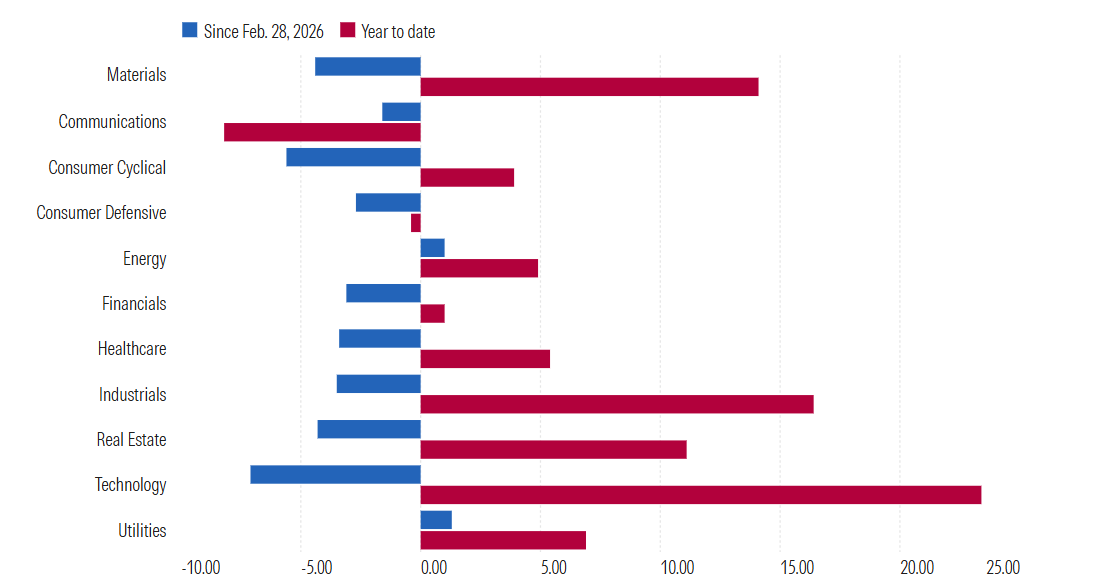

Most Sectors Are Still Up Despite Iran War Selloff

Market-cap-weighted returns

Source: Morningstar Research. Data as of March 6, 2026. Based on the components of the Morningstar TME Asia Index. Download CSV.

China Is Relatively Resilient

While China is the main buyer of Iranian crude and the main market for energy output shipped through the Strait of Hormuz, we think its near-term risk can be relatively well capped, despite higher oil and gas prices.

We understand that China is looking at alternative sources, such as buying more from West Africa, to offset the loss of Iranian supply, and the country still has access to piped gas from Russia. Because China’s power supply continues to be fueled by coal and renewables, which are generally sourced locally, we think the rise in its electricity tariffs can be relatively better contained than those for other Asian countries, which are more reliant on LNG imports and have a market pricing mechanism.